If you have been following Canadian financial news lately, you have likely heard the phrase “mortgage renewal wave” — and for good reason. More than 1.2 million Canadian homeowners are expected to renew their mortgages in 2026, many of them facing monthly payments that are significantly higher than what they locked in during the record-low rate environment of 2020 and 2021.

This is not just a national headline. It is a real and present reality for homeowners, buyers, and sellers right here in Southern Georgian Bay — in Collingwood, The Blue Mountains, Thornbury, Wasaga Beach, and the surrounding communities we call home.

At Keleher + Co. Real Estate, we believe in being transformational, not transactional. That means giving you the honest, data-driven information you need to make confident decisions — whether you are renewing your mortgage, thinking about selling, or ready to buy your next home. This post breaks down everything you need to know about the 2026 mortgage renewal wave and what it means for our local market.

Understanding the 2026 Canadian Mortgage Renewal Wave

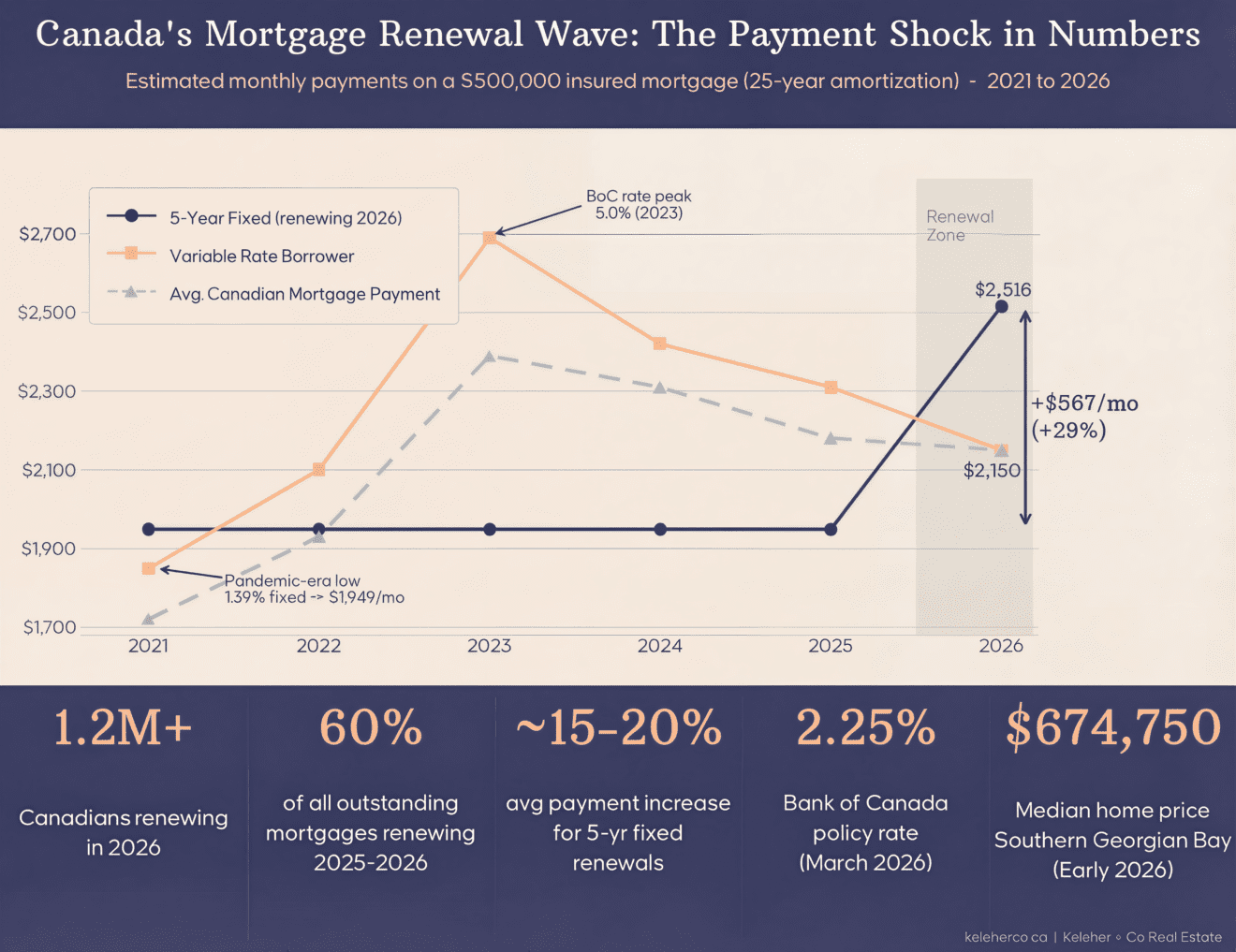

To understand the scale of what is happening, we need to look back at where this all began. During the COVID-19 pandemic, the Bank of Canada slashed its overnight lending rate to near-zero levels to stabilize the economy. The result? Canadians flooded into the housing market with five-year fixed mortgage rates as low as 1.39% and variable rates below 1%.

Those five-year terms are now coming due — and the rate environment today is dramatically different.

According to the Bank of Canada, approximately 60% of all outstanding mortgages in Canada are expected to renew between 2025 and 2026. The CMHC has confirmed that more than 1.5 million households already renewed at a higher interest rate in 2025, and another million are expected to do so in 2026.

The Bank of Canada has held its policy interest rate steady at 2.25% as of March 2026, following a series of cuts that brought it down from a peak of 5% in 2023. While this is welcome news compared to recent highs, it still represents a significant jump from pandemic-era lows. As of late March 2026, the best five-year fixed mortgage rate in Canada sits at approximately 3.69%, and the best five-year variable rate at around 3.30%.

What Does This Mean for Monthly Payments?

The numbers tell a striking story. Consider a homeowner who took out a $500,000 insured mortgage in early 2021 at a five-year fixed rate of 1.39%. Their monthly payment at the time would have been approximately $1,949. At renewal in 2026 at a rate of 3.69%, that same mortgage now costs roughly $2,516 per month — an increase of $567 every single month, or nearly $6,800 per year.

For homeowners with larger mortgages — a common reality in Southern Georgian Bay, where the median residential sale price has hovered around $675,000 to $713,000 in recent years — the payment shock can be even more pronounced.

| Mortgage Scenario | Original Rate (2021) | Renewal Rate (2026) | Monthly Payment Increase |

| $400,000 Mortgage (5-yr Fixed) | 1.39% | 3.69% | ~$450/month |

| $500,000 Mortgage (5-yr Fixed) | 1.39% | 3.69% | ~$567/month |

| $700,000 Mortgage (5-yr Fixed) | 1.39% | 3.69% | ~$790/month |

| $500,000 Mortgage (Variable) | ~0.99% | ~3.30% | ~$490/month |

Estimates based on 25-year amortization and current market rates as of March 2026.

The Bank of Canada’s own analysis found that borrowers renewing a five-year fixed-rate mortgage in 2026 could face an average payment increase of 15% to 20% compared to their December 2024 payment levels. For variable-rate holders, who have already absorbed much of the rate movement, the increase at renewal is expected to be more modest — around 4% on average.

The Stress Beneath the Surface: What the Data Shows

While Canada’s overall mortgage delinquency rate remains relatively low at 0.26%, the picture beneath the surface is more nuanced. According to Equifax Canada, severe mortgage delinquencies — loans more than 90 days past due — rose 30% year-over-year by dollar value and nearly 15% by account count in late 2025.

The stress is most concentrated in markets with the highest home prices. Ontario, in particular, has seen its mortgage delinquency rate climb above 0.3%, driven largely by larger loans above $800,000. This is a critical data point for Southern Georgian Bay homeowners, where property values — especially in waterfront and luxury segments — have historically been well above provincial averages.

That said, the broader consensus among economists and housing analysts is that this is a gradual normalization, not a crisis. As TD Economics noted in March 2026, the average payment increase in 2026 is running at around 6% — down from 10% in 2025 — and the median mortgage payment change is actually near zero, as many short-term fixed-rate holders are renewing into lower rates than they previously held.

How the Mortgage Renewal Wave Is Shaping the Southern Georgian Bay Real Estate Market

The Southern Georgian Bay real estate market has been navigating its own period of recalibration. After the extraordinary pandemic-driven surge of 2020 to 2022, the market has been returning to more familiar, balanced territory. The mortgage renewal wave is one of several factors influencing this transition.

A Market With More Inventory and More Negotiating Power

One of the most visible effects of the renewal wave is an increase in listings. Some homeowners, facing a significant jump in monthly payments, have elected to sell rather than absorb the higher costs. As a result, active listings across the region — spanning Clearview Township, Collingwood, Grey Highlands, the Municipality of Meaford, The Blue Mountains, and Wasaga Beach — remain near a 10-year high, roughly double the inventory levels seen in 2021 and 2022.

This shift in supply has fundamentally changed the negotiating dynamic. Buyers now have more choice, more time, and more leverage than at any point in the past five years.

Prices Have Stabilized, Not Collapsed

Despite the headlines, Southern Georgian Bay has not experienced a housing crash. The year-to-date median residential sale price in early 2026 stands at approximately $674,750, representing a 5% decline from 2025 and well below the 2022 peak of $914,000. Importantly, much of this decline reflects fewer sales in the upper price ranges rather than a broad erosion of property values.

Premium, well-located properties — particularly waterfront homes on Georgian Bay, ski chalets near The Blue Mountains, and move-in-ready homes in Collingwood’s established neighbourhoods — continue to command strong values and attract motivated buyers.

Homes Are Taking Longer to Sell — and That Is Normal

The median days on market in the region has increased to approximately 49 days, compared to just 10 days at the height of the pandemic market in 2022. The current list-to-sale price ratio sits at approximately 95.4%, which is actually consistent with historical norms for a balanced Southern Georgian Bay market.

This is not a sign of distress — it is a return to how real estate is supposed to work. Buyers are conducting proper due diligence, sellers are pricing strategically, and deals are being made based on genuine value rather than fear of missing out.

| Market Indicator | Pandemic Peak (2022) | Current Market (Early 2026) |

| Median Days on Market | 10 days | ~49 days |

| List-to-Sale Price Ratio | 103.5% (over asking) | ~95.4% |

| Active Listings | Historically Low | Near 10-Year High |

| Median Residential Sale Price | $914,000 | ~$674,750 |

| Market Type | Extreme Seller’s Market | Balanced / Buyer-Friendly |

What This Means for Buyers in Southern Georgian Bay

If you have been sitting on the sidelines waiting for the right moment to buy in Collingwood, The Blue Mountains, or anywhere in Southern Georgian Bay, the 2026 market may be the most favourable buying environment in years.

More inventory means more options. Whether you are searching for a ski chalet near Blue Mountain Village, a family home in Collingwood’s Windfall community, a waterfront property on Georgian Bay, or an affordable entry-level home in Wasaga Beach, you will find more properties to choose from than at any point since the pandemic.

Less competition means less pressure. Bidding wars and bully offers are no longer the norm. You have the time to conduct proper home inspections, negotiate on price, and make a decision that is right for your lifestyle and your budget.

Prices have moderated. For buyers who were priced out of the market during the 2021–2022 surge, the current correction has brought properties back into reach. Entry-level homes in the $300,000 to $499,999 range have actually seen a 15% increase in sales activity in early 2026, suggesting that first-time buyers and value-seekers are actively re-entering the market.

The key for buyers in 2026 is preparation. Get your financing in order, understand your budget at today’s mortgage rates, and work with a local agent who knows the micro-markets of Southern Georgian Bay intimately.

What This Means for Sellers in Southern Georgian Bay

For sellers, the 2026 market requires a different mindset than the one that prevailed during the pandemic. The automatic leverage that sellers enjoyed from 2020 to 2022 has faded, and success today depends on strategy, presentation, and realistic pricing.

Homes that are priced accurately from day one, staged thoughtfully, and marketed with a strong digital presence are still selling — and selling well. The list-to-sale ratio of 95.4% means that well-priced homes are achieving close to their asking price. However, properties that are overpriced based on outdated peak-era expectations tend to linger on the market, accumulate price reductions, and ultimately sell for less than they would have if priced correctly from the start.

If you are a homeowner facing a mortgage renewal at a significantly higher rate, it is worth having an honest conversation about your options. In some cases, the most financially sound decision may be to sell your current property and right-size into something that better fits your new monthly budget — whether that means downsizing within Collingwood, exploring a condo in The Blue Mountains, or finding a more affordable lifestyle home in one of the region’s surrounding communities.

5 Smart Tips for Navigating Your Mortgage Renewal in 2026

If you are among the over one million Canadians renewing your mortgage this year, here are five practical steps to protect your financial health:

1. Start Early — Up to 120 Days Before Renewal

Most lenders allow you to begin the renewal process up to four months in advance. Starting early gives you time to shop the market, compare rates, and lock in a rate hold in case rates rise before your renewal date.

2. Do Not Auto-Renew Without Shopping Around

When your current lender sends a renewal letter, do not simply sign it. Lenders typically reserve their best rates for new business, not existing clients. Shopping around — or working with a mortgage broker who can access rates from dozens of lenders — can save you thousands of dollars over your next term.

3. Re-Evaluate Fixed vs. Variable

With the Bank of Canada holding rates at 2.25% and market expectations suggesting rates will remain stable through 2026, the decision between a fixed and variable rate is more nuanced than in recent years. The best five-year variable rate (approximately 3.30%) is currently lower than the best five-year fixed (approximately 3.69%), but fixed rates offer payment certainty. Discuss your risk tolerance and financial goals with a qualified mortgage professional.

4. Consider Your Amortization Period

If your monthly payment increase is significant, extending your amortization period at renewal can reduce your monthly payment — though it means paying more interest over the long run. This is a short-term relief strategy worth discussing with your lender or broker.

5. Align Your Mortgage Renewal with Your Real Estate Goals

Your mortgage renewal is an opportunity to reassess your broader financial and lifestyle picture. If your current home no longer fits your needs — or your new mortgage payments no longer fit your budget — it may be the ideal time to make a move. The Southern Georgian Bay real estate market currently offers excellent opportunities for both buyers and sellers who approach it strategically.

The Bigger Picture: Why Southern Georgian Bay Remains a Strong Long-Term Market

Despite the near-term headwinds of the mortgage renewal wave and broader economic uncertainty, the long-term fundamentals of Southern Georgian Bay real estate remain compelling.

The region continues to attract buyers from across Ontario and beyond, drawn by its four-season lifestyle, proximity to Georgian Bay and the Niagara Escarpment, world-class skiing at Blue Mountain, a vibrant downtown Collingwood, and an increasingly strong local economy. As remote and hybrid work arrangements remain common, the appeal of lifestyle-driven communities like Collingwood and Thornbury has not diminished.

The Canadian Real Estate Association (CREA) forecasts national home sales to grow approximately 7–8% in 2026, with gradual price appreciation returning as buyers re-enter the market. In Southern Georgian Bay, the combination of high inventory, stabilized prices, and easing mortgage rates creates a foundation for a healthy, sustainable recovery — one built on genuine demand rather than speculative frenzy.

For homeowners who purchased during the pandemic peak and are now navigating a higher-rate renewal, the equity they have built — even after the recent price correction — remains substantial. The 2022 median sale price of $914,000 has moderated, but it has not evaporated. Southern Georgian Bay is a market with enduring appeal, and patient, informed homeowners will be well-positioned for the years ahead.

Work With Keleher + Co.: Real Estate Done Differently in Southern Georgian Bay

The 2026 mortgage renewal wave is a pivotal moment for homeowners across Canada — and in Southern Georgian Bay, it is reshaping the real estate landscape in real time. Whether you are renewing your mortgage and wondering whether to stay or sell, looking to buy your first home or recreational property, or simply trying to understand what your home is worth in today’s market, Keleher + Co. Real Estate is here to help.

We are local residents and real estate veterans who know Collingwood, The Blue Mountains, Thornbury, Wasaga Beach, and every community in between like the back of our hands. We bring years of combined experience, a collaborative approach, and a genuine commitment to your long-term success.

Ready to take the next step?

•Request a complimentary market evaluation of your home

•Download our free Buyer’s and Seller’s Guides

•Explore current listings across Southern Georgian Bay

•Connect with our team to get the latest neighbourhood sold data

At Keleher + Co., we are not just here to close a deal. We are here to be your long-term partners in one of the most beautiful and dynamic real estate markets in Ontario.

Sources

[1] Ratehub.ca. “Renewing your mortgage in 2026? Here’s what to expect.”

[2] Ratehub.ca. “Renewing your mortgage in 2026? Here’s what to expect.”

[4] Bank of Canada. “Bank of Canada maintains policy rate at 2¼%.” March 18, 2026.

[5] WOWA.ca. “Best Mortgage Rates Canada.” As of March 25, 2026.

[7] TD Economics. “Mortgage Renewal Mission Possible: The Final Reckoning.” March 4, 2026.